This year began with signs indicating that the Federal Reserve's inflation-fighting tactic was successful in cooling down the hot pandemic housing market.

In Santa Cruz County this year we saw four consecutive months of year-over-year price declines as mortgage rates more than doubled following the Fed's interest rate hikes. This is something the local market hasn't experienced since 2008/2009.

Yet the median price of a single family home increased mont-over-month in April, dipping almost imperceptibly in May. The median home price is projected to increase further as we come into the prime selling season of late spring and summer. This increase, however, will happen at a much more subdued pace than what they market experienced in 2020 and 2021.

One big factor behind the appreciating home prices and the decrease in sales volume -- down 32% in Q1 from a year ago -- is the lack of housing inventory.

“Home sales are bouncing back and forth but remain above recent cyclical lows,” says NAR Chief Economist Lawrence Yun. “The combination of job gains, limited inventory and fluctuating mortgage rates over the last several months have created an environment of push-pull housing demand.”

Housing: Is the housing market going to crash? What experts say about the possibility in 2023.

New construction: The great housing inventory divide: New construction vs existing-homes

Where are home prices headed?

Generally speaking, higher mortgage rates should push home prices downward.

“Yet, housing supply remains so restricted, that any uptick in demand will put upward pressure on prices,” wrote First American Chief economist Mark Fleming in a blogpost. “This is the dynamic that played out in March, as the spring home-buying season ushered in more demand for homes, while insufficient supply prompted buyers to compete and bid up prices.”

Affordability trends in the coming months will depend on mortgage rates and the supply and demand dynamics fueling nominal house price appreciation – dynamics that will play out differently in each market.

“Real estate affordability is local, too,” says Fleming. With median single family prices in Santa Cruz County above $1.3m, and elevated mortgage rates, home buyers are in a tough spot. On top of that wage growth has not kept pace and homeowners insurance rates add to the monthly cost of ownership.

"With 5% down and 7% rates and $600 in non-housing debt, borrowers qualify for these purchase prices if they make above $100,000," Taylor told USA TODAY. "We've seen that buyers are more likely to act when income required to qualify drops below $100k. We need rates in the lower-6% range for this to happen."Taylor expects rates to drop and for inflation to wane this fall.

"So homebuyers shouldn't be discouraged," he says. "Instead, they should get pre-approved by lenders now, and those pre-approvals will only look more attractive as rates drop."

No return to typical seasonality in the market

There will be a lot of uncertainty in the economy over the next few months and prospective home buyers are going to be more opportunistic, as opposed to following traditional seasonal market trends, says Bright MLS Chief Economist, Lisa Sturtevant.

“There will continue to be volatility in mortgage rates as we wait to see what the Fed will do at its upcoming meetings and as we watch economic data roll in over the summer,” says Sturtevant. “Prospective buyers are going to be watching rates closely, and many will try to make an offer on a home when they see rates dip. As a result, we should expect less seasonality this year than we had prior to the pandemic.”

More sellers returning to the market

While inventory will lower than normal this year, we should expect to see more sellers who had been on the sidelines list their home for sale this summer and into the fall.

Many existing homeowners have the "golden handcuffs" of being locked in with incredibly low mortgage rates, which has discouraged discretionary moves.

Some families still have to move due to life circumstances despite rates remaining elevated.

The uptick in new home construction has been minimal, though the various cities in Santa Cruz County are required to add a certain number of units by 2031 as part of the state-required Housing Element.

The bottom line

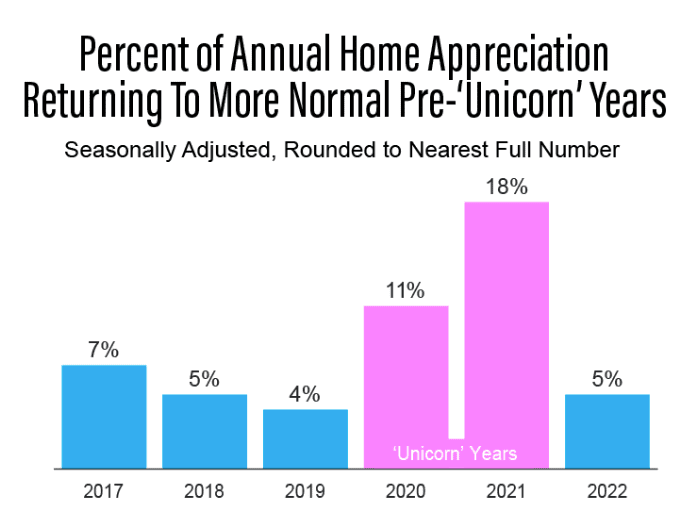

You can't compare today's housing market to the "Unicorn Years" of 2020 and 2021. Comparing housing market metrics from one year to another can be challenging in a normal housing market - and the last few years have been anything but normal.

- While lower than the last couple of years, buyer activity is still stronger than pre-unicorn years.

- Home prices aren't crashing, but we are returning to more normal appreciation.

- While rising, foreclosure filings are still low overall and there is no flood of foreclosures today.

Expect unsettling housing market headlines this year, mostly due to unfair comparisons with the pandemic years.